Often times thought of as a fictional character à la Betty Crocker, Chef Bo-yar-dee was in fact, a real person. Once a head chef at the NYC Plaza Hotel back in the 1920s, Ettore Boiardi, moved to Cleveland, Ohio and opened Il Giardino d’ Italia (Italy’s Garden) —his spaghetti sauce was so iconic at the time, or at least for folks in Cleveland back in 1924, they began asking him for sauce to go, and thus begins our origin story, sauce distributed in milk bottles. In 1927, Boiardi met Maurice and Eva Weiner who were patrons of his restaurant and owners of a local self-service grocery store chain, (we stan independent grocers) the Weiners helped Boiardi bois develop a process for canning the food at scale AND helped them procure distribution across the US through their grocery's wholesale partners (ICONS)

Thus, Boiardi's product soon began to be stocked in markets nationwide and to meet the growing demand, ChefBoi had to open a production factory in Milton, PA where they were now able to grow his own tomatoes and mushrooms. To make it easier for Americans, he anglicized his product’s name to “Boy-Ar-Dee” to facilitate the pronounciation of his actual name, classic USA. The first packaged product was “RTH” (ready-to-heat) spaghettti kit that launched in 1928, which included uncooked pasta, tomato sauce and pre-grated cheese in different containers witihin a box, the vibe was on point IMO, brands could benefit from bringing back this aesthetic, but not you Barilla, you try too fucking hard. Anyways, back to our story—did you know Ettore Boiardi is truly an American hero?

Snaxshot is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Prior to getting into his own restaurant, he worked his way up to head chef at the kitchen of the infamous Plaza Hotel, after having immigrated following his brother Paolo to NYC. Did you know our ChefBoi actually supervised the preparation of the homecoming meal served by Woodrow Wilson at the White House to celebrate 2,000 WWI returning soldiers, Ettore was SERVING, OK! Oh you thought we were done with this part—nope, later on the American military, yes THAT ONE, literally commissioned them to produce rations that would supply Allied troops during WWII, subsequently, he was rewarded TheGold Star, one of the highest honors a civilian can receive, in honor of the company's wartime efforts.

Alas, though life can deal you incredible pasta-bilities, things can quickly go from spaghetti to regret-ti, ChefBoi found himself struggling with cash flow and internal family strains over ownership and direction of the company as they managed rapid internal growth. He was left with the decision to sell his brand to American Home Foods, later turned to International Home Foods, for about $5.96 million, which would later become an incredible profitable investment for AH as Chef Boy-Ar-Dee would become one of the leading canned food brand names in the US. At its highest peak, the company employed almost 5,000 workers that produced 250,000 cans per day.

Post sale ChefBoi remained a spokesperson and consultant for the brand, appearing in many print ads and television commercials from the 1940s through the 60s, with his last appearance in TV commercial being in 1979. Boiardi kept developing new products for them until his demise in 1985, at that time his net worth was estimated at $60 Million, by then Chef Boyardee was grossing $500 Million per year for AH, a company that almost 20 years later would be bought out by a bigger fish, its current snaxdaddy, Conagra brands.

“Hello, may I come in?” says a familiar friendly voice, who would have known at that time, that Ettore Bioardi, hailing from Piacenza in Northern Italy, would become a legend in the grocer-verse, and be welcomed by millions inside their home, across almost an entire century, “My name is Chef Boy-ar-dee!” he exclaims gleefully, but in 2022, ChefBoi, the man, the can, needs no introduction.

Covid, Constraints & Creativity

As was the case of our old ChefBoi, in 2020s, restaurants continue to find success with sales beyond the plate by diving into CPG, but the proliferation of this model in the past couple of years comes after tumultous decades for the industry, even prior to pandemic.

According to industry reports:

—As a result of the COVID-19 pandemic, in the U.S., there was a 66% YOY decline in consumers dining in restaurants during the period of 2020 to Jan. 2021

—By the end of 2020, a National Restaurant Association survey of 6,000 restaurant operators found that more than 110,000 establishments closed permanently or long-term by the end of last year.

—Restaurant industry ended 2020 with total sales that were $240 billionbelow NRA’s pre-pandemic forecast for the year

—Although restaurant and foodservice sales expected double-digit growth in 2021, it wasn’t nearly enough to make up for the substantial losses experienced in 2020

—Majority of permanently closed restaurants were well-established businesses in operation for 16 years; 16% had been open for at least 30 years!

—The Fed raised interest rates 11 times between March 2022 and July 2023 to combat relentlessly high inflation, capital is more expensive then ever, slowing down growth for restaurant chains as investors remain in sidelines.

—That being said, National Restaurant Association is forecasting a record$1.1 trillion in sales in 2024 and the addition of 15.7 million jobs in US.

—According to Technomic data, top 500 restaurant chains increased sales in $31 billion in 2023, up 8% compared to 2022, keeping interest rates high as demand soars.

—People are dining out less frequently. And the NRA reports 51% of adults saying they’re not eating at restaurants as often, 6 % points higher than pre-pandemic.

—By 2025, digital channel sales are expected to account for 30% of total sales for U.S. restaurants.

—Compared to dine-in traffic, digital ordering and delivery have grown 300% faster since 2014.

—Total digital sales of Yum brands, Wendy’s, RBI, and Chipotle totaled $50B in 2023!

—According to Yelp, in the US, diners have taken notice of the rise in self-service options, with spikes in review mentions of "iPad checkout" (up 291%),"ordering kiosk" (up 238%), and “self checkout” (up 235%).

—Technology has become critical and is top investment priority for operators big and small in 2024; 60% of operators plan to make technology investments this year, vs. 48% in 2023

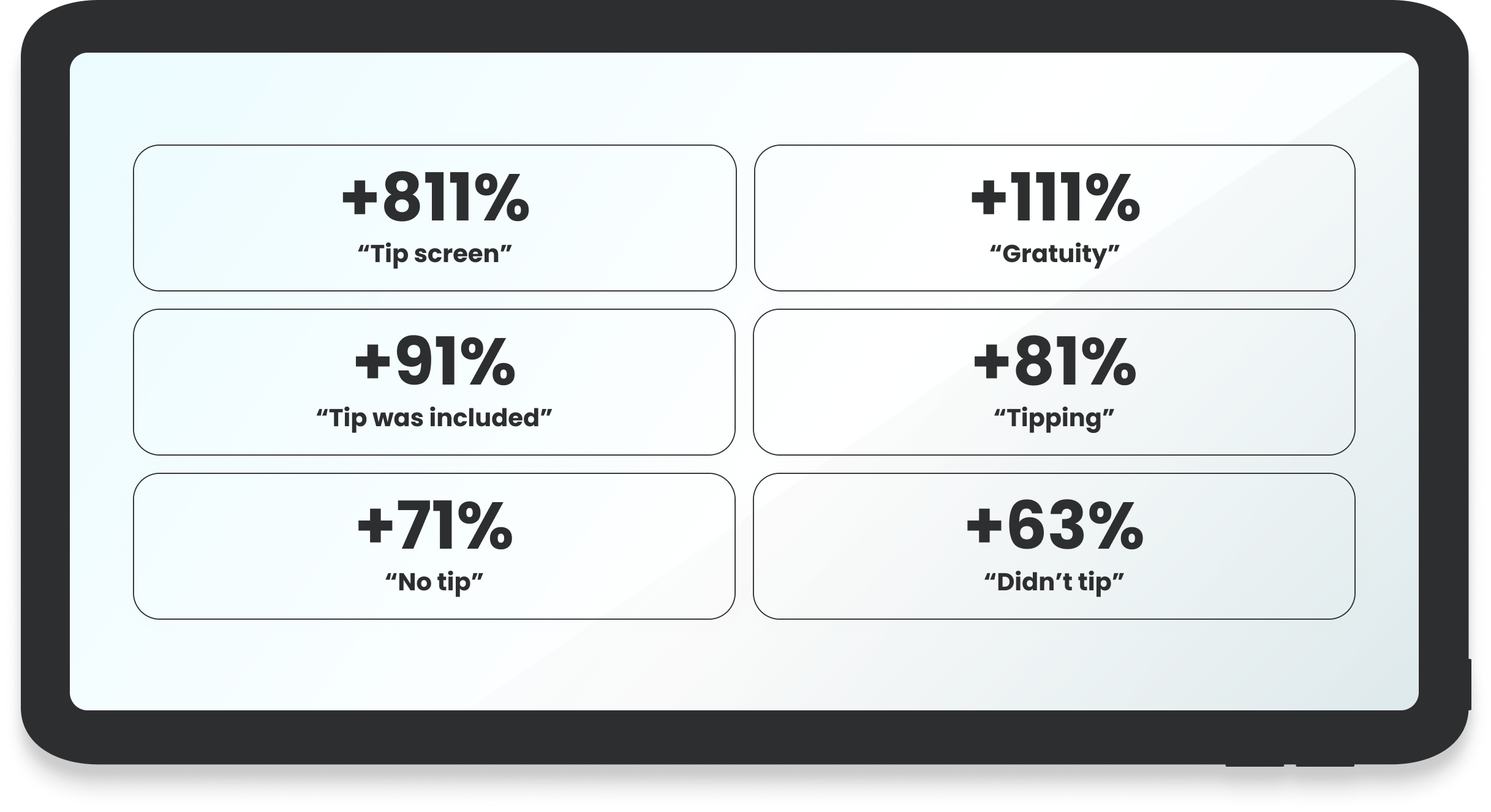

—As digital interfaces replace traditional human service roles, there’s a growing debate among consumers about the necessity of tipping.

Change in gratuity related review mentions on Yelp, May 2023 - Apr 2024 compared to May 2020 – April 2021

Financial health of restuarants

Of all surveyed, over half of restaurant operators said they had relied on savings to offset increased costs, 30% of operators also turn friends and family, the rest applied for loans with smallest percentage resorting to crowdfunding

The labor shortage is also showing signs of easing, with restaurant and accommodation job openings declining from 8.2% in 2022 to 6.7% in August 2023 and the quit rate falling from 5.3% in July 2022 to 3.9% a year later.

If you’ve been able to get this far, you can now understand why in the past couple of years we have witnessed restaurants rush into CPG and retail, for some more established restuarant chains, CPG is more than just a pandemic lifeline for for when in-store sales dropped, it became a core part of their overall growth strategy. Restaurants, once hesitant to lose revenue by selling their products in stores, recognized these products wouldn’t cannibalize their own sales and would actually increase the overall value of their brand.

One way this strategy manifests itself is through brand licensing, which was once an afterthought for many multibillion-dollar food and beverage manufacturers, and has now become into a high paying source of revenue for CPGs that are aiming to grow their business, build equity, and expand a product’s relevancy in an industry that continues to see an explosion of new products and rapidly evolving consumer preferences.

Global sales revenue generated by licensed merchandise and services in food and beverages has steadily climbed from $15.2 billion in 2015 to $16.5 billion in 2019, according to data tabulated by Licensing International.

The industry was responsible for about 6% of the $300 billion in global sales revenue generated in 2019 across all sectors

Expanding restaurant offerings into adjacent food or beverage categories through a new product. These partnerships tend to prioritize generating revenue for a longer period of time while helping to bring lapsed users back to the brand or connect it with new audiences.

Brand licensing is typically faster and less costly than if a company decided to develop a product from scratch, while allowing each partner to piggyback on the benefits of the other — such as a brand name, experience making or marketing a certain product, understanding how to reach a specific consumer and industry connections.

Whether through licensing to SnaxDaddy or investing in facilities to ramp up production, here’s how CPG is helping restaurants break their chains —

90% of restaurant brands in the grocery aisle have entered the retail market during the last six years alone — a trend that shows no sign of abating.

In a 2015 study, GlobalIcons found sales of these products totaled $4.4 billion, and that restaurant brands in stores have exploded from fewer than 10 in 2000 to more than 50.

Chains that license their brand have posted an average 1%-2% increase in same-store-sales in markets where the products are sold.

Cracker Barrel generates 20% of its revenue from its retail segment, according to the chain’s quarterly filings and it continues to expand its retail offerings

Licensed into retail via Valen Group, Red Robin’s fries and onion rings retail sales are now estimated to be more than $40 million annually, with both products leaders in their respective categories.*

Conagra Brands originally held Red Robin licenses, but passed them on to Lamb Weston as part of its 2016 spinoff

Kraft Heinz is among the biggest food companies to tap into the restaurant space through a spate of partnerships with Taco Bell and most recently Benihana.

Kraft Heinz garners immediate benefits from efforts of TGI Fridays, like nationwide advertising campaigns for the restaurant.

It also grants them access to TGI Friday’s production methods and ingredient suppliers for reproducing its most popular items, including favorites like mozzarella sticks, potato skins and chicken wings.

TGI Fridays lineup has been growth spot for Kraft Heinz even as the rest of portfolio suffered from a consumer shift toward natural and better-for-you products, in the last years, TGI Fridays has posted double-digit growth.

Nestlé acquired rights to sell California Pizza Kitchen’s frozen pizzas in 2010 after purchasing license from Kraft as part of a $3.7 billion deal for its pizza business. Since then, brand has remained one of the top 10 frozen pizza brand choices for consumers, though Netslé’s DiGiorno ranks higher.

Retail offered such a lucrative outlet for CPK (specially after filing for bankruptcy) that they began to push out their own products, to Nestlé’s dismay, which they ended up in litigation for.

When Conagra agreed to buy Bertolli and P.F. Chang’s Home Menu frozen meals businesses from Unilever a decade ago, it was closing in on $300M in annual sales.

Chick-fil-A brought their signature sauces to retail shelves in 2020, initially at nearly 1,800 locations in Florida, then rolled out nationally a few months later.

For them retail opportunity creates added brand awareness and a potential to reach new customers, “white space for unit growth” considering they have less than 3,000 restaurants across US, compared to the likes of McDonald’s for ex, at 14,000.

They recently launched their salad dressings in retail stores like Walmart and Kroger.

They’ve opened two full-scale distribution centers to support their growth.

Focus Brands, parent company of Cinnabon and Auntie Anne’s, generates nearly $2 billion in annual retail sales from more than 100 products across its seven brands, and plans to keep growing its retail channel.

Krispy Kreme distributes products to almost 10,000 outlets as of 2022, half that exist outside of the US. Through CPG they see potential to grow that to 50,000.

They updated their business model to involve 120 Krispy Kreme facilities that act as “production hubs,” some of which can deliver products to retailers daily.

According to CEO, through CPG model, they are able to get a 50% increase in price, as people are looking for the best product possible

“We’re really a CPG company with interesting, experiential doughnut shops.”

—Mike Tatersfield, Krispy Kreme CEO

In 2022, despite higher grocery inflation and living in a post-pandemic consumers keep embracing their favorite restaurant brands on retail shelves —and beyond legacy, newer players are starting to ride the CPG wave, leveraging, DTC and retail to cast a wider net beyond their restaurant walls. A trend you can pick up on around the world, from Michelin-star restaurants to hidden gems, here’s a round up of some of our favorite examples on these traversing blurred lines.

Momofuku

Momofuku means lucky peach, and considering David Chang built a 15-restaurant global empire, one could say, it has been a luckyone indeed. Like every restaurant on this track, Momofuku launched a line of chef-approved essentials like soy sauce and a wildly popular chili crunch back in 2020. A bet that would have a lucrative pay off, their pantry staples, priced between $10 to $20, have continously sold out on their website, and are now carried by retailers of all sorts, from the coveted aisles of Whole Foods and Target to trendy curated grocers that have become Pantry KITHs of sorts, their products are available at more than 2,000 retail shelves. Its Goods line has broken records, from becoming the bestselling food launch in the history of wholesaler, Faire or surpassing sales forecasts MoM at Whole Foods.

Though its enjoyed notoriety in retail, its end goal has been to establish Momofuku without having to rely on dine-in, but also being in full control of their relationship with their end consumer, in the same way BigCPG has launched their own DTC efforts, (see Pepsi’s case study with snacks.com) . Though most digitally native brands have begun to pivot outside of DTC, for restaurants it becomes an opportunity to not only sell things faster, but also being able to provide greater context than one can find at your average grocery shelves or even within packaging. Its current CEO Marguarite Mariscal, also notes on how they strategically went about going direct-to-consumer in the first place, by nailing what I like to call, “taste tester fit” —that is they focused on targetting a demographic they already had a relationship with: their followers, their regular customers, keeping it close by first to strengthen position, before looking further ahead.

Little Sesame

Notoriety can help restaurants get a foot in the door as they go the CPG route, but in the case of Little Sesame, would say, that not being notorious for its restaurant has actually proven advantageous to them. If you’re unfamiliar with their fast-casual restaurant, you could easily think Little Sesame is part of the grocer renaissance that is manifested as a myriad of digitally native brands, its beautiful hummus containers have become extremely popular, that they can now be found at the coveted aisles of Whole Foods, top-tier snaxboi territory like Erewhon and Foxtrot and even have distribution partnerships with Sweetgreen restaurant. Little Sesame’s business is currently split evenly between retail and restaurant, but they are looking to make wholesale/grocery the majority of its sales by 2023.

Roberta’s

Roberta’s frozen pizza started an aesthetic movement that has spawned many copycats from around the world over the course of the last decade, and have become a staple at most frozen aisles from the likes of Whole Foods and Foxtrot. In this interview for Heritage Radio, Brandon Hoy, who is one of the owners, recounts what it was like to R&D frozen pizza having to change the original recipe to adapt, on self-distribution, and Whole Foods wanting their products when they first opened a GOWANUS location, a full decade ago now, to getting distributed nationwide, on opting out of USDA because of its insane costs and more, worth a read!

MìLà

One of the most incredible stories in this space, MìLà opened as a brick-and-mortar restaurant a few years ago in Bellevue, Washington by two Chinese American entrepreneurs, Caleb Wang and Jennifer Liao, focused on Chinese street food. Like any other restaurant in 2020, XCJ began to pivot into DTC, much to their surprise, as their products, specially ones not usually prepared for takeout like their soup dumplings, began to take off. With newfound TikTok notoriety, and a growing demand, they began building out a frozen supply chain in order to be able to go DTC, by 2022 MìLà had sold over 13 million dumplings to over 100,000 customers, their revenue saw 5x increase and continues to grow at similar pace.

It comes to absolutely no one’s surprise, that the company would be able to raise $10 Million to further expand into CPG. a raise led by Imaginary Ventures with notorious investors like actor Simu Liu, Magic Spoon’s Gabi Lewis and various veterans in the space. MìLà’s sucess as DTC has brought them back to retail, undergoing a rebrand as they enter the space and further expand distribution and footprint in 2023, with a focus on creating smaller trial packs vrs their current packs, to gain price parity with other similar brands in shelves.

Flour + Water

A staple of San Francisco for more than a decade, award-winning, Flour + Water in San Francisco announced their recent debut of Flour + Water Foods, a modern pasta that blends Italian tradition with Northern California influences. The line offers four boxed dried pastas developed by co-chefs Thomas McNaughton and Ryan Pollnow who bring the craftsmanship of their cuisine to consumers homes. Led by veteran CPG executive, Dan Nestojko (formerly of Bumble Bee foods) the newly created division of the company marks the restaurant’s first consumer retail product, they were able to launch both DTC and in partnership with Whole Foods simultaneously.

Snaxshot is a reader-supported publication. To receive new posts and support my work, consider becoming a paid subscriber.

Tacombi

One of my favorite restaurant goods in terms of packaging, Vista Hermosa is the child of Tacombi, an emerging chain focused on Mexican food, that has done so well they recently received an almost $28 million investment from the likes of Danny Meyer’s, Enlightened Hospitality Investments.

Tacombi's goal over the next five years is to open 75 taquerias.

There are 14 taquerias, soon to be 15 with the opening of their new Miami Beach location, which is set to open next week 12/22.

CPG retail sales are projected to be $10mm in 2022.

Vista Hermosa products are available in over 2000 stores.

Carbone

Carbone is worth mentioning because of its notoriety, though IMO they owe it more to the likes of Nolita Dirtbag than to celebrity spotting, I’ve come to the conclusion that anyone who buys a Carbone sauce jar because they enjoy cooking, is the equivalent of that person who has several KAWS displayed akwardly across their apartment because they have an appreciation of art —according to our followers, real ones go for Rao’s?

And can we take a moment to commemorate the old school, Olive Garden vibe’s Rao’s is still serving in 2022, like they are truly iconic, considering even the likes of Newman’s Own have succumbed to blanding, what the fuck is this?!

Woon

In just a few short years since it opened, Woon Kitchen has evolved into a beloved neighborhood restaurant and a vibrant activist hub, and anyone living in LA or even visiting in LA is familiar with their name, as they’ve become a staple. The son-mom duo who started Woon, have faced enormous obstacles, from Covid to founder Keegan Fong’s mom cancer battle, and it’s such great comfort to know neither were lost. Woon products can be found at shelves of the most trendiest spots like Wine and Eggs, that are much more “in the know” to more widely known as Foxtrot, safe to say they’ve achieved the unthinkable in such an incredible short amount of time, but what makes Woon kitchen and products stand out the most, is their contribution to fighting against Asian hate and create a unique hub, that serves as a niche media platform, highlight their interests as well as artists, community and other makers.

Sweetgreen

Sweetgreen continues to test out CPG from its own products like Crispy Rice Treat and bottling their own hot sauce to collaborations with Siete.

Rubirosa

A staple in Mulberry street since 2009, Rubirosa, like many food joints that spawned around 2010s, benefitted from the advent of foodie culture and the birth of Instagram, to become “iconic” spots that garnered multiple hour long waits at its peak. As with its contemporaries who have equal Gram-fluence, Rubirosa launched an initial pantry product line that includes a marinara inspired by the family's legacy Staten Island pizzeria mother sauce; a vodka sauce which is the restaurant's signature swirled sauce on the Instagram-famous vodka sauce pizza made with an exclusive tomatoes blend, spices and cream and lastly, an extra virgin oil that is the one used in the restaurant's kitchen, originating from Asaro Organic Farm, a fourth generation family farm in Valle del Belice, Sicily. The packaging is a great way to translate that iconic checkered, old-school italian restaurant that adds to that feeling of “restaurant” in one’s pantry.

Milk Bar

Not only a spin off of an already notorious restaurant, Momofuku, but Christina Totsi’s Milk Bar dive into CPG is probably one of the best of this upcoming decade, with their products being remarkably visionary—and have been incredibly succesful. Pre-pandemic, the company had already secured Series B funding in 2019 from the likes of Sonoma Brands, and previously raised Series A from the likes of RSE ventures —but it’s foray into CPG, like many on here, began in 2020, via DTC and doubling down on e-commerce, by 2022 you have 60% of Milk Bar’s sales coming from their site, and their CPG line accounts for 20% of revenue, an increase of almost 10% from 2021. Their products are available on the most exclusive to most accesible shelves around the US, across 7,000 retail accounts, which have continued to grow since the release of their ice cream pints.

BAO

Shing Chung, his wife Erchen Chang and his sister Wai Ting Chung are the trio behind the iconic BAO based in London, England. The team travelled extensively cooking and eating their way across Taiwan and China gaining inspiration for the birth of BAO. After trading successfully in Netil Market in Hackney, the trio opened BAO Soho in 2015 followed by BAO Fitzrovia in 2016; quickly achieving cult status amongst London foodies. In the summer of 2019 they opened BAO Borough, complete with a Karaoke Room. The trio launched their first takeaway-exclusive brand in 2020: Rice Error, notorious for its unique packaging and aesthetic that is reminiscent of vintage 8-bit computers. Cafe BAO, in King’s Cross, and BAO Noodle Shop, in Shoreditch, followed in late 2020 and 2021 respectively.

Their pantry line can be found under Convi (short for convenience) which doubles as their online shop, which they say is “inspired by Seven Eleven.” The store sells a selection of home and lifestyle products, including ceramics, tshirts, candles, and limited edition prints. Convni is also home to BAO’s range of ready-to-drink cocktails and their immensely popular at-home kits, which allow fans to recreate BAO signatures at home. Can only assume England’s restaurants can benefit more of laxer regulations around cocktails-to-go as opposed to broken and outdated system in US. Their pantry staples have taken a life of their own, expanding not only across retail shops in England, but found in curated grocers across Europe, proving to be a succesful extension of the fun and irreverent world they’ve built.

Mum’s

Mum’s Dim Sum is based in Paris and was established in 2012, like Convi and others listed here, their pantry line consists of seasonings and sauces, that extend beyond just their DTC initiatives, but are available at curated grocers across Paris and beyond, to other places in Europe. Its notorious bottles and seasonings are known for their colorful labels.

Chiche

Levinsky’s Deli is the CPG line from famous Israeli restaurant in Paris, Chiche. Their products are sold throughout curated “superettes” and serve as a more casual take on their dining concept, while also allowing for menu favorites to be esasily accesible to customers all around.

Jajaja

Based in Paris, Jajaja is known for its bold neon sign and branding, proper of a modern taqueria in a city oozing sensuality and French cuisine. They have been able to translate this same boldness into their CPG line that is made up of sauces, tortillas, dips and chips, pairs of bold color palettes, with mostly transparent see-thru packaging from the bottles to the bags, allowing for the products’ freshness to shine through–quiteliterally.

El Taco Truck

When I first discovered this brand based in Stockholm, Sweden, it was really hard for me to believe it’s actually a taco truck, lol, and the reason I say this it’s because of how they appear to be in so many retail spots, and not like any other brand that can be found in regular shelf-space, these folks have their own shop within a shop at grocers, where they stock their products, wedged in between their bland competition, like what the fuck?

In case you were wondering, their packaging is a nod to their original pink taco trucks, complete with same neon signs. The food truck to CPG pivot has proven succesful, they’ve even raised from the likes of Nicoya, who has also invested in CPG winners like N!CK’S.

Mama Park

A few years ago Mama Park emerged, in the Doctores neighborhood, a dark kitchen that instantly stole the hearts of all who tried its kimchi. JuHee, better known as Mama Park then expanded in 2021 by opening a restaurant to delight Mexicans with more recipes: Dooriban. Her Kimchi is also become a well known staple across trendy grocers in CMDX, and have since expanded to opening their own adjacent deli/grocer, similar to restaurants like Gjusta, next door, Moa.

Via Carota

Dr. Smood

The wellness café chain has been around for a decade—now setting its eyes on CPG to continue to drive growth. In the span of a year, Dr. Smood has introduced a beverage linealongisde actorMichael B. Jordan as well as recently launched a functional snack bar line, featured alongside its other more staple pantry items like pastas and marinara,gourmet food vs. smart food. This bi-furcated CPG strategy is interesting to me—because each product line is equally complimentary of their morning and afternoon cafés menus, Michelin-Star packaged goods…

Chotto Motto

Tomoya Kawasaki, who co-owns Neko Neko and Wabi Sabi Salon and Dylan Jones, founded Chotto Motto, a unique restaurant packed with pieces of Japanese junk shop treasure, such as instructional children's Sega video games and ’80s pop records, wrapped in the loud and busy murals by local artists Chehehe and Mitch Walder. Their restaurant specialises in the Hamamatsu regional style of cooking gyoza, like others on here, they’ve expanded into kitchen staples, from their famous Yuzu hot sauce to bottling their own sake in an incredibly unique bottle. Their products are available via DTC but also are stocked across shops in Melbourne.

Belle’s Hot Chicken

Started in 2014, inspired by Nashville cuisine, Belle’s Hot Chicken has become a Sydney staple for almost a decade, for all those seeking “southern comfort” style food. As with most of the brand’s featured here, their dive into CPG came out of pandemic, where they were able to leverage their reputation and fun branding and see it yield dividends, as their restaurant products are stocked in the most well known grocers and shops across Sydney.

St. Ali

Since its inception in 2005, ST. ALi has been an industry leader in direct relationships with farmers, in-house roasting, expert coffee brewing, with a best-in-category food offering. Their products are found throughout retail and online shops across Australia, their RTDs, snacks, and coffee products are one of the best known not just in their home turf, but for all those who are “in the know” and can recognized their branding and logo, even behind a product collaboration like the one’s they’ve done with Mr. Black spirits. St. Ali recently opened up a coffee shop in Bali.

Chica Bonita

Similar to OK!, Chica Bonita found that canning their own perfected cocktail could serve as a way to make revenue that was an easy extension of themselves and their experience. Their canned margaritas can be found in retail and online shops across Australia, using their unique and irreverent aesthetic to draw attention in a category that is saturated all around.

NOMA

One of the most notorious Michelin star restaurants, Noma, based in Copenhagen, caused commotion when they announced they would be closing doors, and instead focusing on their growing CPG brand. From corn yuzu hot sauces to wild rose vinegar, the brand recently experienced a rebrand and went from pharmaceutical, to foraging meets apothecary, which seems to be in line with other CPG pantry brands like Acid League and Olea Pia.

Crossing Collaboration Chasm

Moving further along, we are witnessing the era of brands coming full circle, wherein not only are restaurants able to traverse into consumer packaged goods, but extend themselves into places you would never have thought permissible —from art, fashion to media, but before we dig deeper into this, let’s reference McDonald’s. In the past two years, McDonald’s has become the ultimate oxymoron, or a way of affordable affluence, by betting big on strategic collaborations with “in the know” cultural markers —with their latest with Cactus Plant Flea Market capturing world wide attention and nostalgia rush across generations, to their upcoming collaboration with streetwear style icon Nigo.

But to McDonald’s credit, it’s definitely gone through eras where their unique blending of the culture in the moment with their own brand identity have proven succesful, and though you may not be able to get these iconic McDonald cookie boxes at grocers (yet) —judging by their dips into nostalgia like they have done so elegantly with these past collaborations, note, Nigo is hinting at vintage too teasing a video of the oldest McDonald still standing in California—would it not make perfect sense for our ginger McDaddy to explore what it would look like to move their cookies beyond their cafés, even if its just a limited time drop and bring back these iconic packaging that has become as coveted as any Christie’s collectible?

And therefore I say to you, fellow snaxers, the time has come for us to let go of our differences, whether you shop at WAWA or spend a quarter of your yearly income at Erewhon, we must all unite under the banner that is bullying McDonald’s into giving us exactly what we want —snax-as-a-signaler, for fuck sake, even go the General Mills route x KITH(watch out for their incoming Cocoa Puff drop) if needed, but DO SOMETHING, we need these iconic cookie boxes—YESTERDAY!

Beyond this, it should serve as an example of what great marketing and positioning looks like—that in 2022, we have very fashion-forward, “in the know”luxe brands like VAIN collaborating with one of the most available, affordable fast food chains in the world, a juxtaposition of high and low, but in perfect unison, and isn’t that the best thing about creating a unique brand, that no matter in what ways it manifests or extends itself, its core pull remains the same, and those McDonald’s evolution into McDeluxe is one of the most promising shifts of the 2020s.

3Fs: Fast Food Flattery

Another emerging trend in this space, that fits both restaurant to retail is the emerging “fast food flattery” concepts that similar to what artists like Meowulf and Omega Mart have done for the grocery industry, is being replicated as a nod of equal parts reverence and renaissance for legacy fast food chain brands alike.

First up, Mr. Charlie’s— based in both Los Angeles and San Francisco, it became an instant social media favorite after blowing up on TikTok, as every brand and shop aspires to do so in this life time. In full art gallery mode, Mr. Charlie dubs itself an exhibition of plants, a reference to its entire menu being plant-based. It’s packaging is a spoof of McDonald’s and other fast food staple brands like Coca-Cola. Their menu items also take life of their own, The BigChuck for example states “stop staring at me like I’m a piece of meat” obviously in jest, but also maybe there’s more to say on why plant-based meats have to resemble their replacements in the first place?! FUCK, I’m in too deep.

Next up, BJ Novak’s nod to casual food chains that are so ingrained in American culture, his pop-up CHAIN takes from various different elements of these dining staples as you can see from their product packaging as well as their own aluminum water bottle that reads “TAP IS FINE.” CHAIN has also gone to give its own spin to menu staples like the fries sauce caddy packaging (see below) featuring their own sauces as well the ultimate, gag withing the gag, that is partnering with these chain brands themselves, like their most recent one with Taco Bell. Fast food flattery is a reminder of how deeply ingrained these places have become across generations and around the world, and how much of a legacy, even despite the rise of “better for you” movements —they continue to be.

Full Circle

It’s not only restaurants that want to get into retail, we are also witnessing the “reversal” with SnaxDaddy getting into opening ghost kitchens, cafés and even dabbling into restaurants themselves, oldies like from Pepsi, Kellogg’s to Chobani, testing out the waters to see if they can recreate a brand ambiance in the same way the latter has.

Here’s a few examples of how it’s manifesting:

Pepsi, Ghost Kitchens

Last year Pepsi opened a one-month popup Pep’s Place, launched in partnership with Famous Dave’s, had a beverage-first menu that paired Pepsi drinks with food items, as part of marketing “Better with Pepsi”

The virtual restaurant was found at PepsPlaceRestaurant.com and on food-delivery apps such as DoorDash and GrubHub.

The reason behind this became apparent this year, as Pepsi announced it would get into ghost kitchen space via mentoring brands on how to do so under PepsiCo Foodservice Digital Lab.

It will lend its considerable marketing expertise to the effort as well as guidance on technology and menu, including of course, pushing its portfolio brands unto it.

Rumors have it the first of this new portfolio-branded ghost kitchens is launching soon —keep your eyes out for it.

Though Kellogg’s failed at their cereal bar in the US, they’ve seen incredible success in Korea by partnering with local cafés, ice cream shops, and restaurants to do co-branded menu items.

Latest activation saw Kellogg’s take over an entire street in Seoul with trendy cafés, ice cream shops and even over a curated grocer, and translated its brand accordingly within each shop.

It succesffully was able to position themselves beyond their "mascot” driven brand to mesh perfectly with the other brands.

Cosmic Bliss, Scoop Shop

Part of the HumanCo family of brands, Cosmic Bliss opened its first scoop shop in Portland last week as it seeks to become an ice cream parlor that’s equally recognized as their CPG brand.

Cosmic Bliss will serve ice cream sandwiches, shakes, and scoops in a Pearl District shop.

Restaurant-Grocers

The concept of restaurant-grocers isn’t novel of course, but as mentioned way up, we saw the proliferation of this model post-pandemic, and we even included some examples above like Bodega Rita’s and Convi based in London. The US is also seeing a boom in restaurang groups taking a swing at their grocery equivalents, but before we dive into that, let’s talk about the larger manifestation of this trend, that saw a surge in the past decade only to experience a full-stop as soon as COVID began —chef-led restaurant markets.

The 2010s saw the explosion of food halls, pretty sure it can be correlated with rise in foodie culture spread exponetially thanks to Instagram, and some of the most famous examples of thes can be found in New York City:

Eataly

Mostly associated with disgraced chef, Mario Batali, Eataly came to New York City in 2010, garnering incredible press around it.

Since then, the chain has added additional locations in Italy and a few in Tokyo. In 2012 Eataly opened in Rome its largest megastore, in the abandoned Air Terminal building near Ostiense Station.

In September 2022, the UK investment firm Investindustrial VII LP became Eataly's main shareholder by acquiring 52% of its shares for 200 million euros.

Little Spain

Led by the infamous Chef Jose Andres, known for his courages efforts with World Central Kitchen, Little Spain opened at Hudson Yards back in 2019.

In honor of celebrating the “Spanish” way of life, but of course mostly inspired by the success of Mercado San Miguel in actual Spain (Madrid)

Features bars, restaurants, churro stands and of course… a market.

The most recent one to open, via chef Jean-Georges, based in Seaport area it features a mix of restaurant, bars and retail.

But these examples are gargantuan, and not easily replicated, not to mention require an immense amount of capital, time and as the industry quickly realized during pandemic, not easy to pivot when shit hits the roof. Instead, we are seeing the surge of more demure iterations of the restuarant market concept in the US, both in LA and NYC they can be found in—

Gjelina —Gjusta Grocer

Opened back in 2021, Gjusta Grocer is adjacent to their bakery, and it’s been dubbed more expensive than Erewhon, if that is even possible, but it’s a great translation of it’s brand into everything from flowers to produce, not to mention their own line of pantry staples.

You can find all essentials, plus beer and wine and they have their own delivery.

Restaurant to Retail:

If you’ve managed to make it all the way here without somehow succumbing to carpal tunnel, we can go over some key takeaways —

R2R—isn’t new it’s evolving and DTC makes it easy to start (see MìLà) omnichannel is what has proven succesful to withstand test of time

Start local—find taste tester fit, leverage community, those familiar with your brand and grow from there (see Momofuku)

CPG extensions as competitive advantage for restaurants where retail footprint isn’t (see Chick-Fil-A)

From table to pantry —restaurant brands have the potential to become legacy that spans as long as a century (see Chef Boyardee)